Cooperative societies play a major role in helping people save money and access loans in Nigeria. From market women and artisans to civil servants and small business owners, cooperatives provide a structured but flexible way to pool resources and support members financially. To understand why cooperatives work and where problems sometimes arise, it is important to understand how they manage savings and loans behind the scenes.

What a Cooperative Society Is

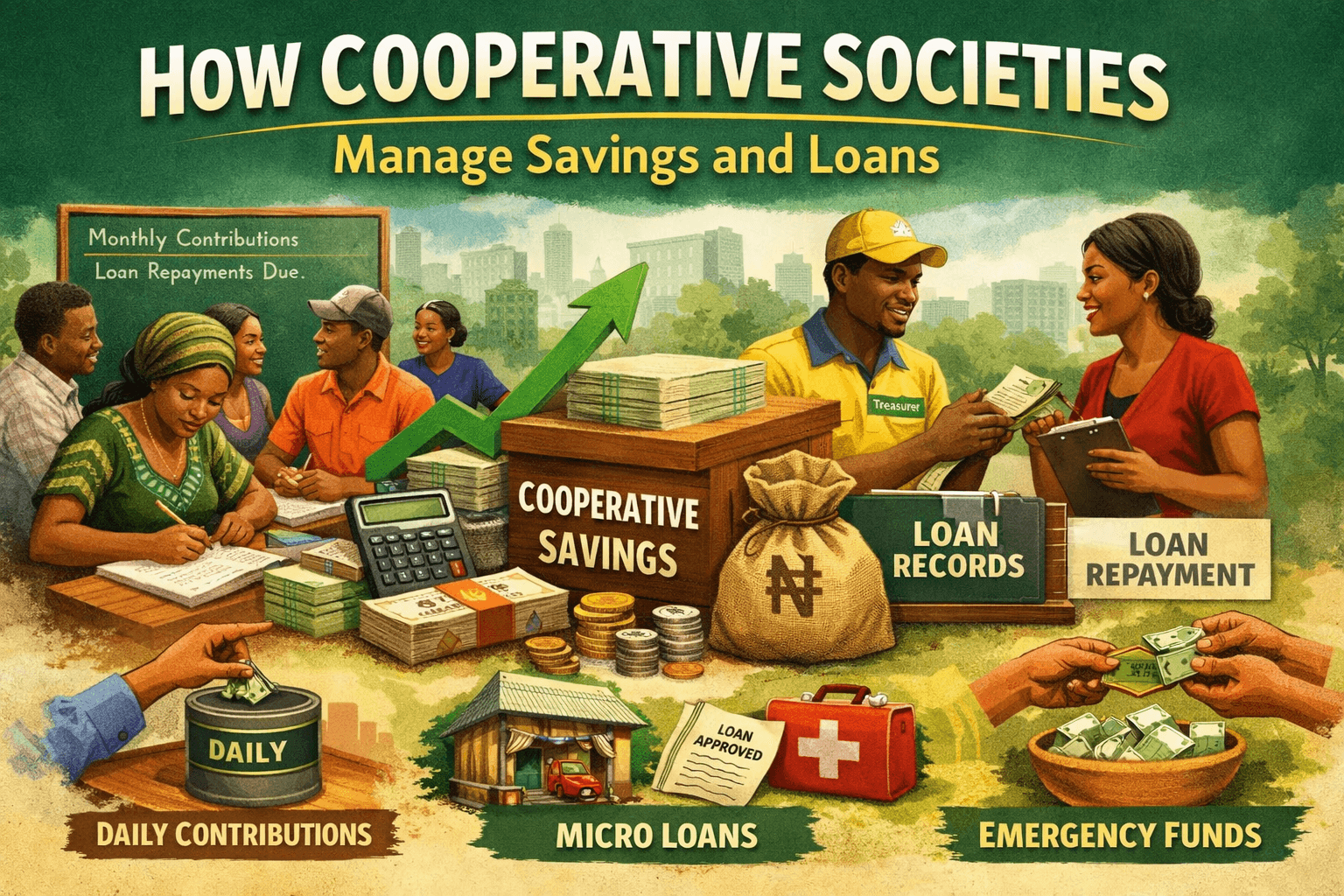

A cooperative society is a member-owned financial group formed to meet the economic needs of its members. Members contribute money regularly, and the pooled funds are used to give loans to members at agreed terms. Unlike banks, cooperatives are usually community-based and operate on trust, shared rules, and collective responsibility.

How Savings Are Collected

Savings are the foundation of every cooperative society. Without consistent savings, there can be no loans.

Most cooperatives collect savings in one or more of the following ways:

Monthly contributions where members pay a fixed amount every month

Weekly or daily contributions common among traders and artisans

Voluntary savings where members save extra money when they can

The amount each member contributes is usually agreed upon at the beginning and documented in the cooperative’s constitution or bylaws. Some cooperatives allow members to increase their savings over time, while others require a fixed amount for fairness.

Savings are often recorded in:

- Passbooks

- Digital spreadsheets

- Accounting software

- Manual ledgers

Proper record-keeping is important. Each member’s savings balance must be clearly tracked to avoid disputes later.

Where the Money Is Kept

Once savings are collected, cooperatives store the funds in different ways depending on their size and structure.

Common options include:

- A cooperative bank account

- A microfinance bank account

- A licensed cooperative bank

- Combination of cash holdings and bank deposits

Well-managed cooperatives avoid keeping large amounts of cash. Funds are usually deposited into a bank account that requires multiple signatories, such as the chairman, secretary, and treasurer. This reduces the risk of misuse.

How Loan Requests Are Made

Members do not automatically qualify for loans just because they save. Most cooperatives have a loan application process.

Typically, a member must:

- Have saved consistently for a minimum period

- Fill a loan request form

- State the loan purpose

- Agree to repayment terms

Some cooperatives limit loans to a multiple of the member’s total savings, such as two or three times the saved amount. This protects the cooperative from heavy losses.

How Loans Are Approved

Loan approval is usually handled by:

- A loan committee

- The executive council

- The general meeting

The approving body considers:

- The member’s savings history

- Past loan repayment behavior

- The purpose of the loan

- The cooperative’s available funds

Approval is rarely automatic. In strong cooperatives, decisions are documented and communicated transparently to avoid favoritism.

Interest Rates and Charges

Unlike commercial banks, cooperative societies charge lower interest rates. The goal is to support members, not maximize profit.

Interest may be charged:

- Monthly

- Flat-rate on the loan

- On a reducing balance

The interest earned is often used to:

- Grow the cooperative’s funds

- Cover administrative costs

- Pay dividends to members at year-end

Some cooperatives also charge small processing or documentation fees.

Loan Disbursement

Once approved, loans are disbursed in one of the following ways:

- Bank transfer

- Cash payment

- Cheque

Members usually sign a loan agreement that states:

- Loan amount

- Interest rate

- Repayment schedule

- Penalties for default

This agreement protects both the cooperative and the borrower.

How Loan Repayment Works

Loan repayment is one of the most important aspects of cooperative management.

Repayment methods include:

- Monthly deductions from salary

- Cash payments during meetings

- Bank transfers to the cooperative account

Repayments are tracked carefully. Missed payments are noted immediately to prevent problems from escalating.

Some cooperatives allow grace periods, while others apply penalties for late payments. These penalties discourage defaults and protect other members’ savings.

How Defaults Are Handled

Loan default is one of the biggest risks cooperatives face. To manage this, cooperatives rely on multiple safeguards.

Common methods include:

- Guarantors from within the cooperative

- Using the member’s savings as collateral

- Peer pressure and group accountability

- Legal action as a last resort

In many cases, a defaulting member’s savings are withheld until the loan is settled. Guarantors may also be asked to repay if the borrower fails.

Profit Sharing and Member Benefits

At the end of the financial year, cooperatives often calculate their surplus. This comes from:

- Interest on loans

- Registration fees

- Penalties

The surplus may be:

- Shared among members as dividends

- Added to reserve funds

- Used for cooperative projects

Members with higher savings usually receive higher dividends, which encourages consistent contributions.

Common Challenges in Cooperative Loan Management

Despite their benefits, cooperatives face challenges such as:

- Poor record-keeping

- Favoritism in loan approval

- Loan defaults

- Weak leadership

- Lack of financial transparency

When these issues are not addressed early, they can cause mistrust and eventual collapse of the cooperative.

What Makes a Cooperative Successful

Successful cooperative societies share common traits:

- Clear rules and constitution

- Transparent leadership

- Strong record-keeping

- Strict loan recovery processes

- Active member participation

When members understand how savings and loans are managed, trust grows and the cooperative becomes stronger.

Final Thoughts

Cooperative societies succeed because they are built on collective effort, trust, and discipline. Savings provide the foundation, while loans offer members the opportunity to grow financially. However, the system only works when rules are respected, records are accurate, and leadership is accountable.

Understanding how cooperative societies manage savings and loans helps members make better decisions and avoid common pitfalls. When properly managed, cooperatives remain one of the most effective grassroots financial systems in Nigeria.