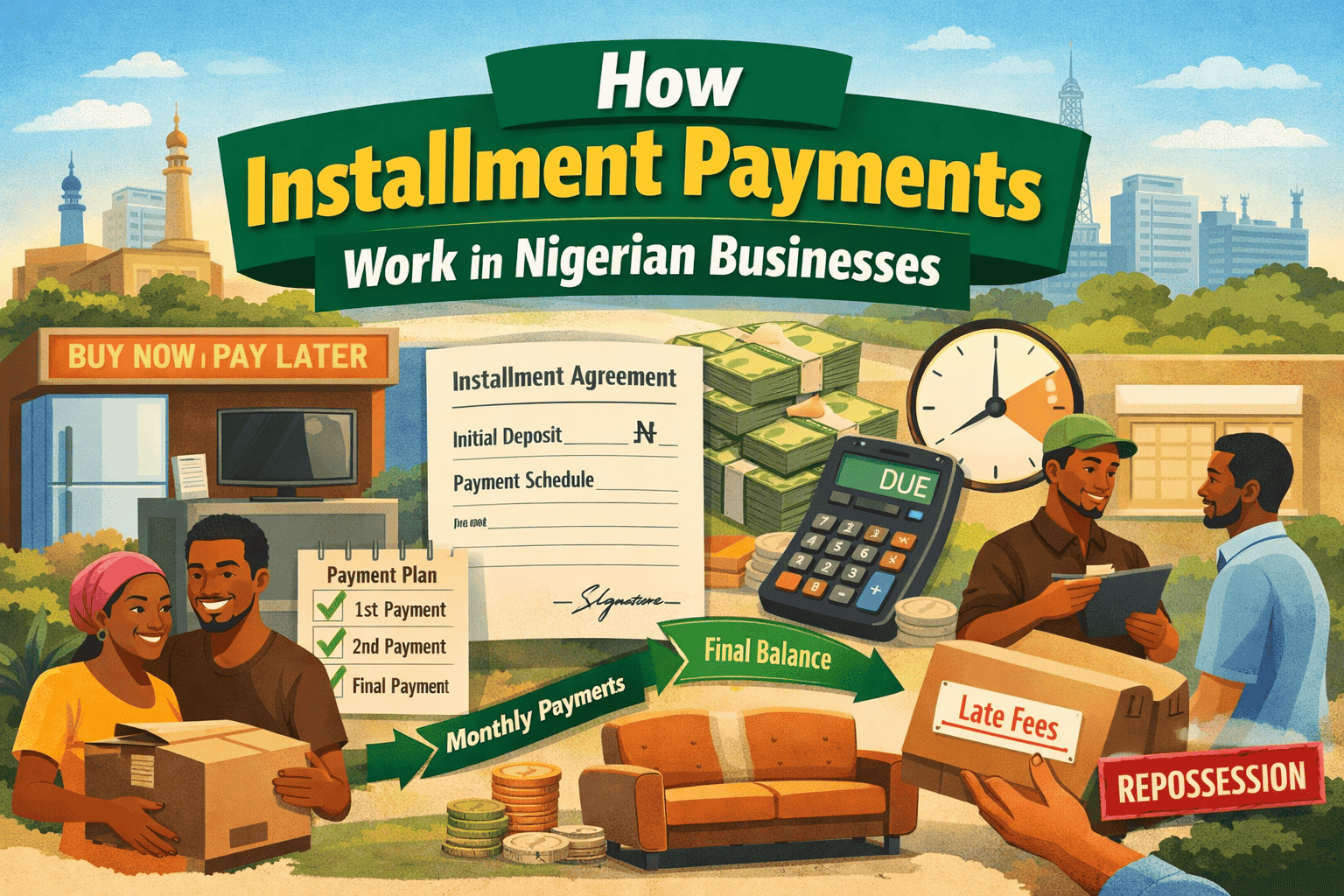

Installment payments are a common way of doing business in Nigeria. From electronics shops and furniture dealers to real estate companies and informal traders, many businesses allow customers to pay for goods or services gradually instead of making one full payment at once. This system helps buyers afford items they may not be able to pay for immediately, while sellers attract more customers and increase sales.

Understanding how installment payments work in Nigerian businesses can help you avoid misunderstandings, hidden costs, and unnecessary disputes.

What Installment Payment Means

An installment payment is a payment arrangement where the total cost of a product or service is divided into smaller amounts, paid over a specific period. Instead of paying everything upfront, the buyer agrees to pay in parts according to an agreed schedule.

In Nigeria, installment payments are used for items such as land, houses, phones, electronics, school fees, household equipment, and even some services.

Why Nigerian Businesses Use Installment Payments

Many Nigerian businesses adopt installment payment systems because of economic realities. A large number of customers earn income daily, weekly, or monthly and may not have access to credit facilities from banks.

Offering installment payments helps businesses:

-

Reach more customers who cannot pay at once

-

Increase sales volume

-

Build long-term customer relationships

-

Stay competitive in crowded markets

For customers, installment payments reduce financial pressure and make big purchases more manageable.

Common Types of Installment Payment Systems in Nigeria

There are different ways installment payments are structured, depending on the business and the item involved.

One common type is the fixed installment plan. In this system, the buyer pays a fixed amount at regular intervals, such as weekly or monthly, until the full amount is completed. This is common with electronics, furniture, and school fees.

Another type is the deposit-and-balance system. Here, the buyer makes an initial deposit, often between 20% and 50% of the total price, and then pays the remaining balance over an agreed period. This is very common in land and real estate transactions.

There is also the flexible installment system, often used by informal businesses. Payments are not strictly fixed, but the buyer pays whenever money is available, as long as progress is being made. This system relies heavily on trust.

How Prices Are Set for Installment Payments

In most Nigerian businesses, installment payments cost more than outright payments. This is because sellers factor in risks such as delayed payments, inflation, and the time value of money.

For example, a product that costs ₦100,000 outright may cost ₦120,000 when paid in installments over six months. The extra amount covers:

-

Risk of default

-

Inflation

-

Administrative costs

-

Opportunity cost of not receiving full payment immediately

Some businesses clearly state this difference, while others quietly increase the price without explaining it. Buyers should always ask for the total amount payable before agreeing.

How Payment Schedules Are Structured

Payment schedules vary widely in Nigeria. Some businesses prefer monthly payments because many people earn salaries monthly. Others prefer weekly payments, especially in markets and informal settings.

A typical installment agreement will state:

-

Total cost

-

Initial deposit

-

Amount to be paid per period

-

Payment frequency

-

Duration of payment

-

Consequences of default

In formal businesses, this is written down. In informal businesses, it may be agreed verbally, which often leads to disputes later.

What Happens When Payments Are Delayed

Delayed payments are one of the biggest challenges of installment systems in Nigeria. When payments are late, businesses may respond in different ways.

Some businesses charge penalties or late fees. Others extend the payment period but increase the total amount. In informal settings, sellers may simply apply pressure through constant reminders or community influence.

In more structured businesses, especially real estate, failure to meet payment deadlines can lead to forfeiture of deposits or cancellation of the agreement, depending on the contract.

Ownership and Possession During Installment Payments

Ownership rules during installment payments depend on the type of item and agreement.

For movable items like phones or electronics, some sellers allow the buyer to take possession immediately but retain ownership until full payment is made. Others keep the item until payment is complete.

For land and property, possession is often delayed until a significant percentage has been paid. Documents are usually released only after full payment is completed.

Understanding who owns the item during the payment period is critical to avoiding loss.

Role of Trust in Installment Payments

Trust plays a major role in Nigerian installment payment systems, especially in informal businesses. Many agreements are based on personal relationships, referrals, or community reputation.

This trust-based system works well when both parties are honest, but it also creates room for abuse. Sellers may change terms mid-way, while buyers may deliberately delay payments.

Formal businesses try to reduce this risk by using written agreements, receipts, and sometimes guarantors.

Common Mistakes People Make

One common mistake buyers make is not asking for a written breakdown of payments. Another is assuming that missed payments will not have consequences.

Sellers also make mistakes, such as releasing goods or documents too early or failing to properly document agreements.

Both parties often underestimate how inflation and income instability can affect long-term payment plans.

How to Protect Yourself in Installment Deals

To protect yourself, always ask for:

-

The total amount payable

-

A clear payment schedule

-

Written proof of every payment

-

Clear terms for default or delay

If the transaction is large, such as land or property, ensure agreements are documented properly and reviewed by someone knowledgeable.

Final Thoughts

Installment payments are an important part of how Nigerian businesses operate. They help bridge the gap between limited income and rising costs, but they also come with risks.

Understanding how installment payments work, how prices are calculated, and what happens when payments are delayed can help both buyers and sellers avoid unnecessary conflicts. When properly structured and clearly understood, installment payments can be beneficial to everyone involved.