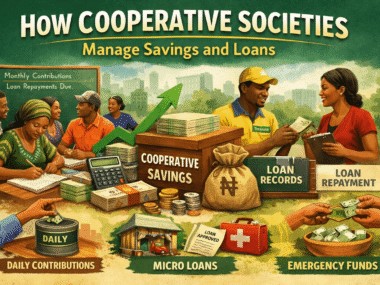

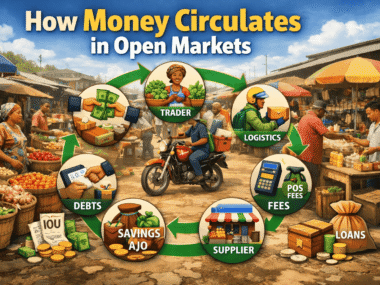

Daily contribution, popularly known as ajo or esusu, is one of the oldest and most trusted informal savings systems in Nigeria. Long before banks and mobile apps became common, people used ajo to save money, access lump sums, and support one another financially. Even today, traders, artisans, salary earners, and small business owners still rely on this system.

This article explains how daily contribution works, why people use it, and what to watch out for.

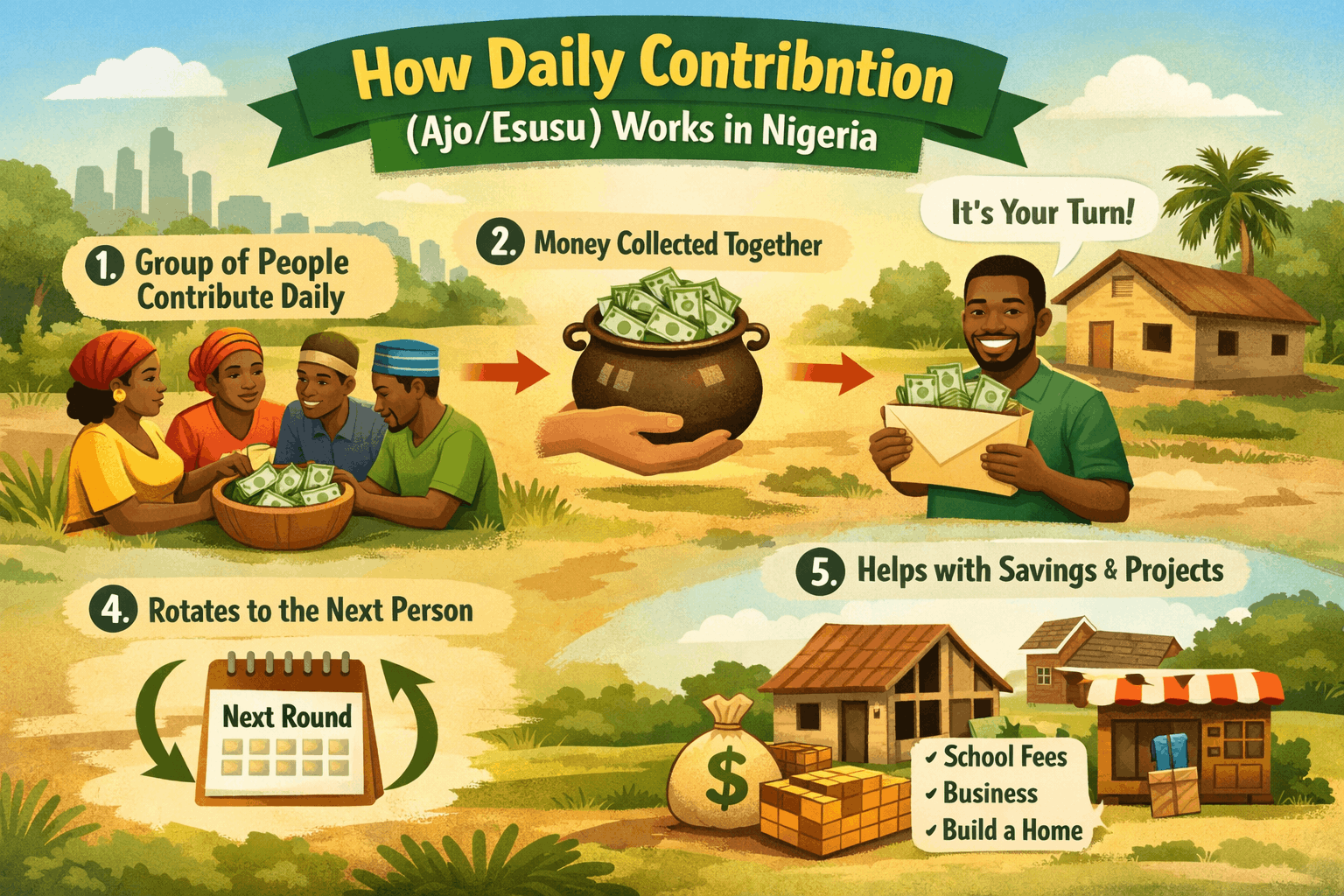

What Is Daily Contribution (Ajo/Esusu)?

Daily contribution is a rotational savings system where a group of people agree to contribute a fixed amount of money regularly—usually daily or weekly—and take turns collecting the total sum.

In many cases, a collector (also called an ajo collector or esusu agent) moves around daily to collect money from participants. At the end of an agreed period, each contributor receives a lump sum equal to the total of everyone’s contributions for one cycle.

The system is based on trust, consistency, and community reputation, not formal contracts.

How the Daily Contribution Process Works

The process usually follows a simple structure.

First, a group of people or individuals agree on a fixed daily amount, such as ₦500 or ₦1,000. This amount remains the same throughout the cycle.

Second, contributors decide the duration of the contribution. A common structure is 30 or 31 days, especially for daily contributors like traders.

Third, the collection order is agreed upon. In group ajo, each person knows the day they will receive the bulk money. In collector-based ajo, individuals usually collect their total at the end of the cycle.

Fourth, the collector visits contributors daily to collect the agreed amount and records payments in a notebook or card.

At the end of the cycle, the contributor receives their lump sum, minus the collector’s fee if applicable.

Types of Ajo/Esusu in Nigeria

There are different ways ajo operates depending on location and arrangement.

Group-Based Ajo

This involves a group of people who contribute together. Each person collects the total contribution once during the cycle. For example, if 10 people contribute ₦1,000 daily for 10 days, each person will receive ₦10,000 on their assigned day.

This type relies heavily on mutual trust, as someone who collects early could default later.

Collector-Based Ajo

This is common in markets and among small business owners. A collector moves around daily to collect money from individuals. At the end of the month, the contributor receives their total savings, minus a service charge.

In many cases, the collector’s fee is one day’s contribution, meaning if you save ₦1,000 daily for 30 days, you receive ₦29,000.

Workplace or Association Ajo

Some workplaces, trade unions, or associations run internal ajo systems. Contributions may be daily, weekly, or monthly, and the structure is often more organized.

Why People Use Daily Contribution

Despite the availability of banks, many Nigerians still prefer ajo for several reasons.

One major reason is forced discipline. Knowing that someone will come to collect money daily encourages consistency.

Another reason is easy access. No paperwork, no bank forms, and no minimum balance are required.

Ajo also helps people raise lump sums quickly for rent, school fees, business stock, or emergencies.

For many small traders, ajo separates business money from personal spending, helping them avoid touching their savings.

How Ajo Collectors Make Money

Ajo collectors earn by charging a service fee. The most common method is taking one day’s contribution from each participant per cycle.

For example, if a collector manages 50 people saving ₦1,000 daily, the collector earns ₦50,000 at the end of the cycle.

Collectors also rely on reputation and trust. Once a collector is known to be reliable, more people join, increasing their income.

Common Risks and Challenges

While ajo is useful, it is not without risks.

The biggest risk is default. In group-based ajo, someone who collects early may stop contributing later.

Another risk is collector disappearance. Since the system is informal, a dishonest collector could abscond with funds.

There is also no legal protection in most cases. If something goes wrong, recovery can be difficult.

Poor record-keeping can also cause disputes, especially when payments are not properly tracked.

How People Reduce Ajo Risks

To reduce risks, many contributors join ajo schemes run by well-known collectors with long-standing reputations.

Some groups require new members to collect last, ensuring they prove consistency before receiving money.

Others use daily cards, receipts, or digital records to track payments clearly.

In some communities, social pressure and reputation act as strong enforcement tools.

Ajo vs Formal Banking

Unlike banks, ajo:

-

Does not pay interest

-

Has little or no regulation

-

Relies on trust instead of contracts

However, ajo offers:

-

Convenience

-

Flexibility

-

Strong savings discipline

Many Nigerians use both systems together, saving small amounts through ajo while using banks for larger or long-term savings.

Final Thoughts

Daily contribution (ajo/esusu) continues to thrive in Nigeria because it fits the realities of everyday income earners. It is simple, flexible, and built on community trust.

However, participants should understand how it works, recognise the risks, and choose arrangements carefully. When done properly, ajo remains a powerful financial tool that helps people save, plan, and meet important financial goals.